Introduction

In an era of accelerating global green transitions, the competition for critical raw materials—essential components for electric vehicles (EVs), batteries, renewable energy, and digital tech—has intensified geopolitical dynamics. Morocco, with its vast mineral reserves and strategic geography, has emerged at the intersection of this competition. As China deepens its investment in Moroccan mining and manufacturing, and the EU strives to secure footholds in global mineral supply chains, analyzing the intricate Moroccan–Chinese–European triangular relationship provides critical insight into the evolving green economy. This essay explores the historical background, current partnerships, strategic interests, challenges, and future outlook defining this complex nexus.

For more: https://africaciviclens.com/

Morocco’s Mineral Wealth and Strategic Position

Morocco stands at the forefront of the global energy transition not only due to its progressive policy frameworks and foreign partnerships but also thanks to its abundant mineral wealth and highly strategic geographic position. As nations race to secure reliable sources of critical raw materials—vital for renewable energy infrastructure, electric vehicles (EVs), and advanced battery technologies—Morocco’s resource base and connectivity give it unique leverage in shaping the future of green industry.

A. Phosphate Dominance

One of Morocco’s most powerful assets is its unrivaled dominance in phosphate reserves. The country controls approximately 70–75% of the world’s known phosphate rock reserves, primarily located in the Khouribga and Bou Craa regions. These reserves are managed by the state-owned OCP Group, one of the largest phosphate producers globally. Morocco has long been a global leader in phosphate exports for agricultural fertilizers, which form the backbone of food production worldwide.

In recent years, however, phosphate’s strategic significance has expanded beyond agriculture. With the emergence of lithium iron phosphate (LFP) batteries, particularly favored for electric vehicles and stationary storage systems, phosphate has gained renewed geopolitical importance. LFP batteries are known for being safer, more stable, and cheaper to produce compared to nickel-based alternatives. Major EV manufacturers, especially in China, are accelerating their transition to LFP battery chemistry—significantly boosting the demand for processed phosphate derivatives like iron phosphate (FePO₄). Morocco, therefore, is not only exporting traditional fertilizers but also increasingly contributing to the battery value chain, positioning itself as a core supplier in the global green transition.

B. Polymetallic Resources

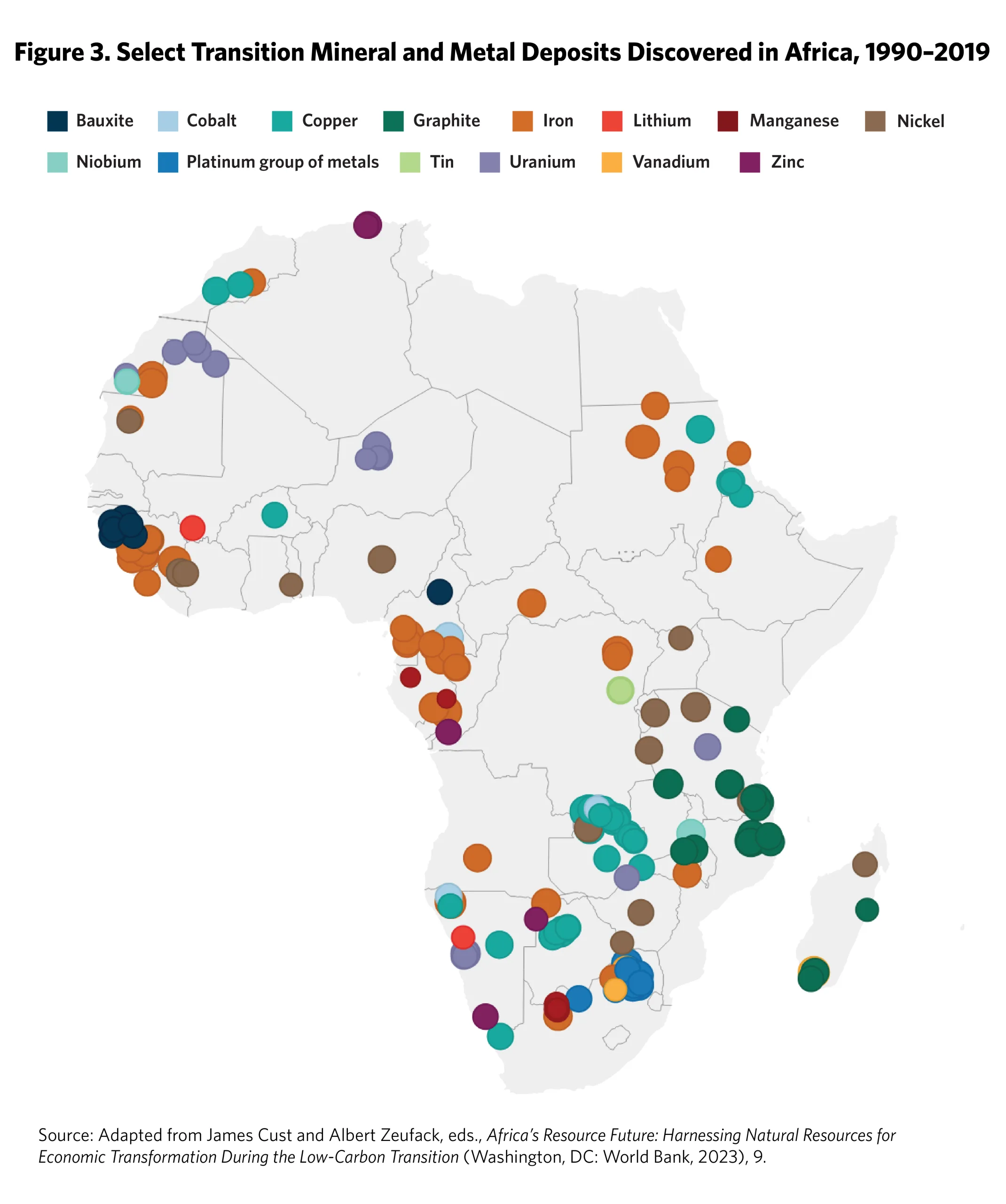

In addition to phosphate, Morocco is rich in a diverse portfolio of critical and strategic minerals, including cobalt, copper, manganese, silver, lead, zinc, and barite. These minerals are essential for a variety of clean energy technologies, including wind turbines, solar panels, and EV batteries. According to geological surveys and industrial reports, Morocco is among Africa’s top producers of silver, zinc, and cobalt.

The country is actively scaling up its production capacities to meet global demand. A notable project includes a cobalt sulfate production plant, scheduled to begin operations in 2025, which will yield 5,800 tonnes of cobalt sulfate annually—a key input for lithium-ion battery cathodes. In parallel, Morocco is investing in copper refining and manganese processing infrastructure, aiming to move up the value chain from raw extraction to downstream industrial transformation. These initiatives align with Morocco’s broader strategy of leveraging its resource endowment for industrial development rather than relying solely on raw material exports.

C. Strategic Location and Infrastructure

Morocco’s geostrategic location at the crossroads of Europe, Africa, and the Atlantic makes it a natural logistics and trade hub. Situated just 14 kilometers from Spain across the Strait of Gibraltar, Morocco offers rapid maritime access to European markets. This proximity is further enhanced by Morocco’s free trade agreements with both the EU and the U.S., allowing goods manufactured or processed in Morocco to enter Western markets with reduced or zero tariffs.

Additionally, Morocco has invested heavily in world-class infrastructure to facilitate trade and industrial growth. The Port of Tangier Med, one of Africa’s largest and most technologically advanced ports, serves as a vital logistics center, connecting Moroccan exports to over 180 global ports. Complementing this are high-speed rail networks, expanding automotive and aerospace industrial zones, and renewable energy megaprojects that provide competitive green electricity for industrial use.

Together, these factors make Morocco not just a mineral-rich country, but a strategically positioned platform for energy transition industries, attracting investment from global players seeking sustainable, efficient, and geopolitically stable supply chains.

.

Deepening Morocco–China Partnership

A. Belt and Road Expansion

- Morocco signed onto China’s Belt and Road Initiative (BRI) in 2022, becoming the first North African country to formalize a BRI cooperation plan Observer Research Foundation.

- Through the Digital Silk Road, Chinese firms including Huawei, ZTE, and PowerChina have placed billions into Moroccan solar plants, highways, and smart infrastructure Chatham House+3Observer Research Foundation+3Observer Research Foundation+3.

B. Investments in Green Minerals and EV Batteries

- Chinese material manufacturers like BTR, Gotion, CNGR, BYD, Qingdao Sentury, Youshan, and others have pledged US $8–10 billion into Morocco’s battery chemistry and EV‑related facilities POLITICO+3Observer Research Foundation+3flanders-china.be+3.

- Key projects include:

- A €300 million BTR cathode factory near Tangier with 50,000 t/year capacity Reuters+1flanders-china.be+1.

- A $1.3 billion Gotion gigafactory targeting 20 GWh/year, expected around 2026 flanders-china.be.

- A $2 billion CNGR plant in Jorf Lasfar and other initiatives tapping Morocco’s reserves and trade perks Morocco World News.

C. Strategic Bypass of Trade Barriers

- Chinese firms are leveraging Morocco’s free trade access to the EU and U.S. to circumvent tariffs such as the 100% U.S. EV duties and ~38% EU provisional duties, avoiding direct shipment from China Wikipedia+6flanders-china.be+6POLITICO+6.

- This “nearshoring” model allows China to produce within Morocco for export, maintaining access to Western markets The Maghreb Times !+3POLITICO+3Observer Research Foundation+3.

3. European Union’s Green Partnership Strategy

A. EU–Morocco Green Partnership (2022)

- In October 2022, the EU launched its first Green Partnership with Morocco, aiming to align with the European Green Deal through cooperation on energy, climate, environment, and green economy Enlargement and Eastern Neighbourhood+2Enlargement and Eastern Neighbourhood+2Climate Action+2.

B. Funding the Green Transition

- In March 2023, the EU pledged €624 million to Moroccan initiatives including agriculture, forestry, green entrepreneurship, and climate resilience Enlargement and Eastern Neighbourhood.

- Germany separately entered a climate and energy alliance with Morocco to develop green hydrogen production and export—one project aims for 10,000 t/year of green hydrogen Reuters.

C. Reducing EU Dependency on China

- Via the 2023 Critical Raw Materials Act, the EU plans to achieve by 2030: 10% domestic mining, 40% processing, and 25% recycling of critical materials Transnational Institute+2Wikipedia+2Reuters+2.

- 2025 saw the EU commission approval of 13 overseas critical-material projects, aimed at diversifying supply away from China’s dominant position Reuters.

4. Intersections and Strategic Tensions

A. Competing Alliances in the Supply Chain

- The Chinese-led model emphasizes rapid infrastructure and processing build-out, often under looser environmental standards, positioning Morocco as a Chinese export hub .

- Meanwhile, EU efforts focus on ensuring secure, sustainable, and socially responsible critical mineral supply—seeking cooperation with Morocco, yet wary of dependency Wikipedia.

B. Economic and Industrial Implications for Morocco

- Foreign investment has strengthened Morocco’s green-transition sectors but carries dependency risks, particularly in roles like raw-material supplier or “assembly hub,” with limited domestic value capture .

- For example, promises of 30,000 jobs from Gotion may lean heavily on subcontracted and low‑wage labor, raising concerns about equitable development Morocco World News.

C. EU’s Strategic Safeguards

- EU bloc aims to avoid repeating Chinese dominance by diversifying sources—supporting projects in Greenland, Serbia, Malawi—and leveraging financing through the Minerals Security Partnership Financial Times.

- EU-Morocco cooperation on green hydrogen and sustainability signals intent to integrate Morocco into a greener, multi-partner energy future Observer Research Foundation+9Reuters+9Enlargement and Eastern Neighbourhood+9.

5. Challenges and Risks

A. Governance and Environmental Oversight

- Chinese projects may prioritize speed over environmental or social safeguards, possibly leaving Morocco with ecological or social downsides .

- Morocco must reinforce regulations, labor protections, and community engagement to ensure a “just” green transition.

B. Economic Diversification and Value Capture

- Risk exists that Morocco might be boxed into low-value functions (mining/refining), without developing local R&D, engineering, or high-skilled manufacturing sectors.

- Upgrading value chains will require domestic policies that promote technology transfer, local innovation, and incentive structures.

C. External Political Pressures

- Morocco must navigate US–EU–China geopolitics: Chinese investment can bring benefits, but may complicate EU relations or trigger Washington response under policies like the IRA or security review of foreign direct investment .

Strategic Pathways Forward

As Morocco becomes a critical node in the global green transition value chain, the country faces both exceptional opportunities and significant strategic risks. The influx of foreign investment from both China and the European Union (EU), primarily in the electric vehicle (EV) and battery mineral sectors, could boost Morocco’s industrial and economic development. However, capitalizing on this promise demands more than mineral wealth and geographic luck—it requires coherent national strategies to promote sustainable, inclusive growth. The following pathways can help Morocco assert greater control over its natural resources, maximize domestic value, and avoid structural dependency in an era of intensifying geopolitical competition.

A. Strengthening Moroccan Policy Instruments

To ensure that the green transition translates into long-term prosperity and resilience, Morocco must build a solid regulatory and institutional foundation for managing its mineral and industrial assets.

First and foremost, Morocco should strengthen its mineral governance framework, which includes establishing transparent licensing procedures, anti-corruption mechanisms, and long-term environmental safeguards. These steps are critical to attracting high-quality foreign investors while minimizing environmental degradation and social unrest. A national critical minerals strategy—aligned with global best practices—could serve as the backbone for regulating exploration, extraction, and post-processing activities.

Second, robust environmental impact assessments (EIAs) and social performance requirements should be mandated for all major mineral projects, especially those led by foreign investors. Morocco can draw on examples like the EU’s Corporate Sustainability Due Diligence Directive (CSDDD) or Canada’s mining ESG requirements to ensure that green minerals are not extracted at the expense of communities or ecosystems.

Moreover, local content mandates must become a priority. These require foreign companies to procure a portion of services, labor, and materials from domestic firms or workers. Such policies not only promote local economic activity but also prevent Morocco from being relegated to low-value positions in the global supply chain. Countries like Chile, Indonesia, and South Africa have used similar instruments to varying degrees of success.

Additionally, Morocco should establish clear investment screening rules to safeguard national interests, particularly in sectors involving strategic minerals or advanced battery technology. With the proliferation of Chinese investments across the Moroccan battery and EV space, the country needs mechanisms to review deals on security, environmental, or economic grounds—just as the EU Foreign Direct Investment (FDI) Screening Regulation or U.S. CFIUS mechanisms do.

To enhance global integration, Morocco must also align with international norms on sustainability, traceability, and human rights. Meeting EU regulations such as the Carbon Border Adjustment Mechanism (CBAM) and the Critical Raw Materials (CRM) Act would not only improve Morocco’s credibility as a supplier but also provide preferential access to premium green markets. Compliance with traceability standards, carbon intensity benchmarks, and ethical sourcing rules could set Moroccan exports apart in an increasingly values-driven global economy.

Furthermore, to institutionalize these priorities, Morocco should create a Critical Minerals Coordination Agency or similar regulatory body to manage inter-ministerial cooperation, engage foreign investors, enforce standards, and monitor compliance. Such an agency could also act as a one-stop shop for companies seeking clarity on rules and incentives, reducing bureaucratic friction while maintaining strategic oversight.

B. Driving Local Value Addition

One of the central challenges for Morocco in the global green transition is avoiding the “resource trap,” where countries export raw materials while importing high-value products. To combat this, Morocco must prioritize domestic value addition across the green minerals and energy value chain.

This begins with a decisive policy shift from extractivism to industrial upgrading. Morocco should implement incentive frameworks to attract processing facilities, battery component plants, cathode/anode factories, and eventually full battery assembly or EV manufacturing. Tax breaks, land grants, and customs exemptions could be tied to technology transfer, local hiring quotas, or training investments. Industrial parks near ports and renewable energy hubs like Jorf Lasfar, Tangier, and Laâyoune can be developed into specialized green-tech zones.

Equally important is the establishment of research and development (R&D) centers dedicated to battery chemistry, mineral refining processes, and green materials innovation. These institutions could be created through public–private partnerships involving Moroccan universities, state-owned enterprises (like OCP or MASEN), and international firms. Research hubs would not only anchor local expertise but also help develop homegrown technologies suited to Moroccan conditions—such as low-cost solar thermal storage or phosphate-based battery chemistries.

Another crucial step is aligning the education and vocational training system with emerging green industries. Curricula in engineering, environmental science, geochemistry, and data analytics should be modernized and expanded to equip Moroccan youth with the skills needed to thrive in battery, EV, and renewable sectors. Programs like Germany’s dual training system or Finland’s battery school initiatives could offer models for Moroccan adaptation.

To deepen value addition, Morocco must also support the creation of local supply ecosystems—including SMEs, logistics firms, equipment manufacturers, and digital services—that are integrated into global EV and battery supply chains. Special funds and preferential procurement programs can help nurture these enterprises and link them with larger multinational players.

If successful, this approach could turn Morocco from a supplier of raw cobalt or phosphate into a producer of battery-grade chemicals, functional components, and clean energy solutions, significantly increasing export revenues, industrial capabilities, and domestic employment.

C. Diversified Global Engagement

In a multipolar world where supply chain geopolitics increasingly shape trade and investment flows, Morocco must pursue a balanced foreign policy that extracts maximum benefit from its partnerships without falling into dependency traps.

Morocco’s current relationship with China offers rapid capital inflows, manufacturing expertise, and technology, especially in battery materials and EV assembly. However, overreliance on Chinese financing and technical dominance poses long-term strategic vulnerabilities, especially given rising global concerns over China’s near-monopoly in critical minerals.

To mitigate this, Morocco must actively diversify its global engagement, strengthening strategic ties with the EU, U.S., Canada, Australia, Japan, and other democratic partners. The EU, for example, has committed to forming Critical Raw Materials Partnerships with resource-rich nations. Morocco could position itself as a preferred partner through joint exploration, shared R&D, and co-financed industrial projects.

Partnerships with the Minerals Security Partnership (MSP)—a U.S.-led initiative to build secure and resilient critical mineral supply chains—could provide an alternative source of funding and reduce overdependence on Chinese capital. Similarly, EU-backed investment platforms like Global Gateway and development banks such as the EIB can be leveraged to co-finance infrastructure, processing plants, and training programs.

Importantly, Morocco should push for more joint ventures (JVs) between Chinese and Western firms operating on Moroccan soil. For example, a joint battery cell plant between Gotion (China) and BASF (Germany) could ensure knowledge sharing, transparency, and dual-market access. These hybrid partnerships offer a buffer against the risks of foreign monopolization while encouraging innovation.

Additionally, Morocco should explore membership or observer status in global governance frameworks like the OECD Mining Framework, the Extractive Industries Transparency Initiative (EITI), and International Energy Agency (IEA) critical minerals forums, which can enhance technical cooperation and policy credibility.

This diversified engagement strategy is not just economic—it is geopolitical. It allows Morocco to assert its strategic autonomy in a fragmented global order while avoiding binary alignment with either the West or China. In doing so, Morocco can become a neutral platform for global green transition collaboration, a role increasingly valuable in today’s polarized environment.

Morocco’s green minerals sector sits at the confluence of global energy transition, industrial reshuffling, and geopolitical rivalry. To navigate this landscape successfully, the country must upgrade its regulatory structures, push for domestic value capture, and maintain a multi-aligned international strategy. The choices made today will define whether Morocco emerges as a mere transit zone for foreign interests—or a sovereign, sustainable leader in the green industrial age.

Conclusion

Morocco stands at a crossroads: a pivotal green‑transition node connecting Chinese manufacturing imperatives and EU energy-security strategies. With unparalleled resource endowments, strategic geography, and burgeoning infrastructure, it offers unparalleled potential. Yet realizing this potential depends on Morocco’s ability to secure equitable, environmentally sound, and innovation-driven development amid superpower competition.

China seeks to embed its industrial model via rapid capital deployment and export-led assembly. The EU, meanwhile, prioritizes secure, sustainable, and diversified supply chains. Morocco’s success will rely on its capacity to leverage these dynamics, institutionalize governance, upgrade domestic value chains, and act as a strategic partner to multiple global actors—ultimately defining its place in the green energy landscape.

External Links for Further Reading

- “Morocco–China’s Gateway to the European Union” – Maghreb Times

- “The Digital Silk Road in Morocco” – ORF-India

- “Critical Raw Minerals in Morocco” – Transnational Institute

- “Will Morocco become a battleground in a global trade war?” – Chatham House

- “EU and Morocco launch first Green Partnership” – European Commission

- “Germany, Morocco agree alliance on green hydrogen” – Reuters

- “China EV battery maker BTR to build cathode plant in Morocco” – Reuters

- “EU picks 13 new critical material projects” – Reuters

- “Report: Morocco’s green minerals boom may entrap nation…” – Hespress EN

- “China’s Backdoor: How Morocco Became Key in the Battery Trade War” – Morocco World News

The post by: https://afripoli.org